Oreninc Index Update: March 13, 2017

ORENINC INDEX sees strong pullback as gold tests $1,200 USD

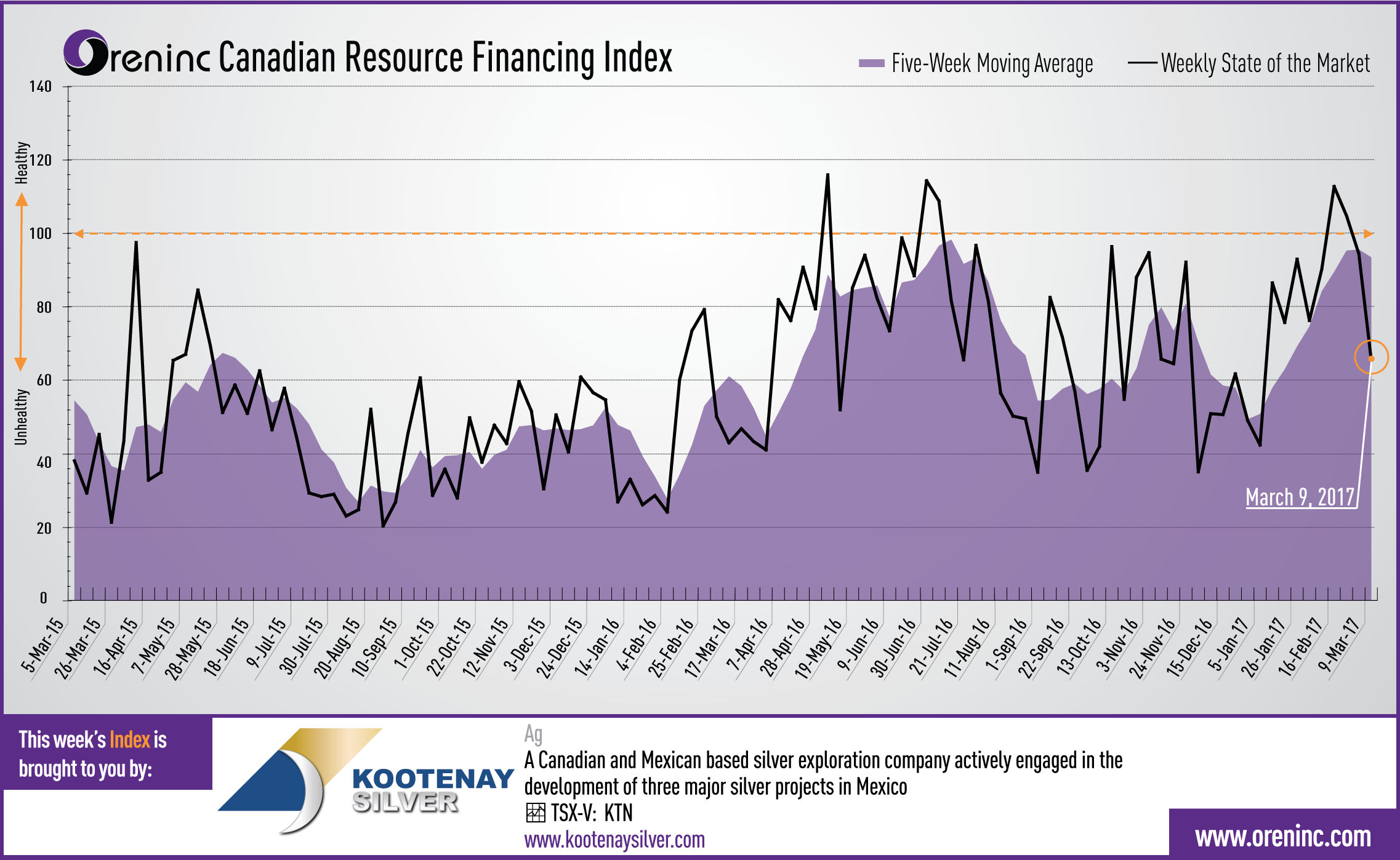

ORENINC INDEX - Monday, March 13, 2017

North America’s leading junior mining finance data provider

Follow us on facebook and find us on Twitter @Oreninc

AuRico Metals Corp. (TSX: AMI): Completed acquisition of Kiska Metals

Kootenay Silver Inc. (TSXV: KTN) new Oreninc sponsor

Last week index score: 94.43

This week: 65.62

The Oreninc Index saw a strong pullback in the week ending March 9, 2017 to 65.62 from 93.45 the previous week as gold pulled back and fell below the $1,200 USD per ounce before closing the week at $1,204 USD.

The first quarter of the year is traditionally the strongest financing window of the year, with deals dropping off in March after the PDAC (Prospectors and Developers Association Conference) in Toronto, and this year is playing out true to form. Total fund raising dollars announced fell significantly to C$97.1m from C$285.5m, a nine-week low, which included five brokered financings for a total of C$25.1m within which was one bought-deal financing for C$4.0m. The average offer size fell to a nine-week low as well, to C$2.1m from $6.5m, whilst the total number of financings announced increased slightly to 47, a two-week high. As a footnote, financings and therefore the Oreninc Index has historically experienced a hard fall in early March—what many people refer to as the PDAC hangover or PDAC curse—and usually recovers sometime in April.

With gold having a weak week, the industry’s leading benchmark index, the van Eck GDXJ continued to retrench and is now up just 9.95% so far in 2017. In line with the gold pullback, the SPDR GLD ETF gold inventory sold of 825.22 tonnes, its lowest volume since February 6, 2017.

Despite strikes at three of the world’s largest copper mines (Escondida in Chile, Grasberg in Indonesia and as of Friday 10 March, joined by Cerro Verde in Peru) the copper price weakened to close at $2.60 per pound. With the Escondida strike passing thirty days (longer than the 25-day stoppage in 2006), management is now making overtures to the strikers to come to terms. Before these strikes, many copper analysts were forecasting copper to enter supply deficit in 2017.

It is not just gold and copper that are down: WTI crude took a sharp drop and fell below $50 USD for the first time since December 2016.

The Dow Jones Industrial Average continued above the 20,000 mark and coming off a record 21,155 the previous week to close at closing at 20,902. The S&P/TSX Composite Index also continues at near historic high levels but down slightly on the prior week at 15,506.

The past week saw the behemoth PDAC conference that brought together over 24,000 people from the juniors, mid tiers and majors, finance people and suppliers. Attendance was up a couple of thousand over 2016 and juniors expressed greater optimism. Many have been able to finance in recent weeks and have sufficient cash for 12-18 months’ work. One takeaway is that money is starting to trickle down to explorers and not just in low political risk jurisdictions such as Canada and the US. There was standing room only in the presentations by Argentina, Ecuador and Colombia showing that appetite for risk is starting to return.

Whilst at PDAC, Oreninc also sat down with The Mercenary Geologist Mickey Fulp to record Podcast #4 in the ongoing series, to get his observations on the event, which will be available on www.oreninc.com shortly.

Financial news highlights

GoldQuest Mining Corp. (TSXV: GQC) announced and closed a strategic investment by Agnico Eagle Mines (TSX: AEM) via a non-brokered private placement of 38.1M shares at a price of C$0.60 for a total investment of C$22.86M that saw Agnico take a 15% stake in the explorer. The proceeds will be primarily used for exploration and development of properties in the Tireo Belt in Dominican Republic.

Highland Copper Company Inc. (TSXV: HI) (the “Company”) increased the size of the non-brokered private placement it originally announced in Novermber 2016 to up to 265.0M units at a price of $0.10 per unit. The original C$17M raise has been increased to $26.5M. The company expects to close a final tranche of the placement by March 17. So far the company has issued 49.4M units under the first and second tranches that closed on November 30, 2016 and February 22, 2017. Highland intends to use the proceeds to update the feasibility study on its Copperwood project, to complete the acquisition of the White Pine project and to settle its liabilities.

Summary:

- Number of financings increased to 47, a two-week high

- Five brokered financings were announced for $25.1m, a nine-week low.

- One bought-deal financings were announced for $4.0m, a two-week high.

- Total dollars decreased to $97.1m, a nine-week low.

- Average offer size lower to $2.1m, a nine-week low.

Major Financing Openings:

- Goldquest Mining Corp. (TSXV:GQC) opened a $22.86 million offering on a strategic deal basis.

- Renaissance Oil Corp. (TSXV:ROE) opened a $10 million offering underwritten by a syndicate led by Haywood Securities on a best efforts basis. Each unit includes one warrant that expires in 27 months. The deal is expected to close on or about March 29, 2017.

- White Gold Corp. (TSX-V:WGO) opened a $10 million offering underwritten by a syndicate led by GMP Securities on a best efforts basis. The deal is expected to close on or about March 21, 2017.

- Goldstrike Resources Ltd. (TSX-V:GSR) opened a $6.03 million offering on a strategic deal basis. Each unit includes one warrant that expires in 48 months.

Major Financing Closings:

- Itafos (TSXV:IFOS) closed a $45.93 million offering underwritten by a syndicate led by Raymond James on a best efforts basis.

- Goldquest Mining Corp. (TSXV:GQC) closed a $22.86 million offering on a strategic deal basis.

- Ascendant Resources Inc. (TSXV:ASND) closed a $20.04 million offering underwritten by a syndicate led by Eight Capital on a best efforts basis. Each unit includes a 1/2 warrant that expires in 60 months.

- IDM Mining Ltd. (TSX:IDM) closed a $15.25 million offering on a strategic deal basis.

Company news

AuRico Metals Corp (TSX: AMI) C$1.00, Mkt Cap C$149.7 million

-

Completed acquisition of Kiska Metals Corp.

-

Kiska's royalty portfolio consists of six royalties including on the East Timmins and Boulevard properties operated by Kirkland Lake Gold and Independence Gold

-

Kiska's six exploration projects present organic royalty creation opportunities.

-

AuRico now has a portfolio of 17 royalties

AuRico Metals is a mining development and royalty company the gold-copper Kemess property in British Columbia, Canada that hosts the feasibility-stage Kemess Underground project and the Kemess East exploration project. AuRico's royalty portfolio includes a 1.5% NSR royalty on the Young-Davidson gold mine and a 2% NSR royalty on the Fosterville mine.

Conclusion: The Kiska Metals acquisition provides royalty diversification and long-term growth potential through assets located in North America. It also sees the company grow its exploration portfolio in British Columbia within relative proximity to Kemess.

Kootenay Silver Inc. (TSXV: KTN) C$0.30, Mkt Cap C$51.5 million

Oreninc welcomes Kootenay Silver as a sponsor. Kootenay is an exploration company with projects in the Sierra Madre region of Mexico and in British Columbia, Canada. Its leading properties are the La Cigarra silver project and the Promontorio Mineral Belt, in Chihuahua, Mexico and Sonora, Mexico. La Cigarra hosts a resource estimate of 18.54Mt containing 51.47Moz of silver in the Measured & Indicated categories grading 86.3 g/t Ag & 4.45Mt tonnes containing 11.46Moz Ag in the Inferred category grading 80 g/t Ag. The Promontorio mineral belt includes the La Negra high-grade silver discovery and its Promontorio silver resource that is under option to Pan American Silver. The Promontorio silver resource hosts a resource estimate of 44.5Mt containing 92Moz AgEq in the Measured & Indicated categories grading 64.3 g/t AgEq & 14.6Mt containing 24.3Moz AgEq in the Inferred category grading 52 g/t AgEq.

Comments