ORENINC INDEX down as bought deals fall away

ORENINC INDEX - Monday, September 9th 2019

North America’s leading junior mining finance data provider

Sign up for our free newsletter at www.oreninc.com

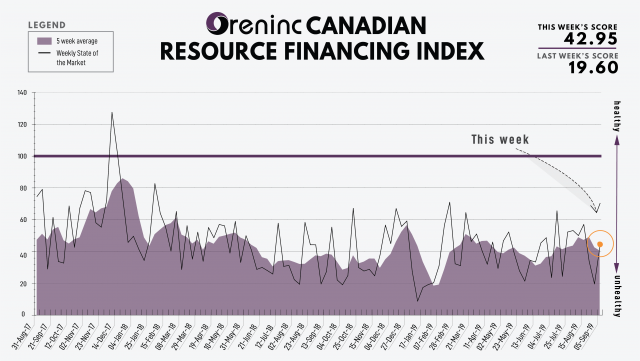

Last Week: 19.60 (updated)

This week: 45.04

Oreninc is at the Precious Metals Summit in Beaver Creek. Email us to arrange a meeting.

The Oreninc Index more than doubled in the week ending September 6th, 2019 to 45.04 from an updated 19.60 as the number of deals increased and the aggregate amount announced more than tripled, despite it being a shortened week due to the Labor Day holiday.

This week sees the North American precious metals world descend on Colorado for the Precious Metals Summit in Beaver Creek to be followed by the Denver Gold Forum in Denver.

The emerging gold bull looked as though it would enter conference season at a gallop with the gold price around US$1,550/oz but the last two days of the week saw it crash back close to $1,500/oz having experienced its biggest daily dollar loss in three years after the US and China said they would work on new trade talks and stronger than expected US private sector employment data. Gold continued to suffer the following day as the service sector recovered from nearly three-year lows in August, according to the Institute of Supply Management as the Non-Manufacturing Purchasing Managers Index rose to 56.4%. This pushed back gold’s attempt to rally after the US Bureau of Labor Statistics jobs report showed the country created fewer jobs than expected in August as nonfarm payrolls rose by 130,000. US unemployment remains unchanged at 3.7%.

Speaking in Switzerland, US Federal Reserve chairman Jerome Powell poured cold water on gold with comments that the US economy will continue to grow even as it faces global headwinds. The Fed is due to hold its next Federal Open Market Committee meeting on 17-18th September with broad expectations of another cut in interest rates to be announced.

Following weeks of protests, Hong Kong’s leader Carrie Lam withdrew from a proposed law to allow the extradition of Hong Kong citizens to mainland China.

After the week the new UK prime minister Boris Johnson has just had looking to take the nation out of the European Union, one can understand why he didn’t want the job when his leave campaign won the referendum vote in 2016. His first efforts at leading the country were all met with rejection as he was defeated in three-successive votes in Parliament and opponents to the UK leaving the EU without a deal at the end of October successfully mustered a bill to stop this possibility. The EU then rejected the solution Johnson offered to prevent a hard border being put in place between the Republic of Ireland and Northern Ireland.

On to the money: total fund raises announced more than tripled to C$69.3 million, a three-week high, which included one brokered financing for $10.1 million, a two-week high and one bought-deal financing for $10.1 million, also a two-week high. The average offer size more than doubled to $2.9 million, a two-week high, while the number of financings increased to 24.

Gold saw a mixed week peaking at US$1,542/oz before closing down at $1,520/oz from US$1,526/oz a week ago. The yellow metal is up 18.55% so far this year. The US dollar index showed strength as it closed up at 98.91 from 97.64 last week. The Van Eck managed GDXJ saw some profit taking as it closed down at US$41.05 from $$41.22 a week ago. The index is now up 35.84% so far in 2019. The US Global Go Gold ETF closed up at US$17.39 from US$16.95 a week ago. It is up 52.41% so far in 2019. The HUI Arca Gold BUGS Index closed up at 228.24 from 226.21 last week. The SPDR GLD ETF saw its inventory take a significant jump to 878.31 tonnes from 859.83 a week ago after hitting a mid-week high of 882.41 tonnes.

In other commodities, silver continued its recent tear by adding the best part of another dollar to close up at US$18.38/oz from $17.43/oz a week ago. Copper continues in the doldrums as it closed up at US$2.55/lb from $2.53/lb a week ago. Oil continues to suffer as well as WTI closed up at US$55.10 a barrel from $54.17 a barrel a week ago.

The Dow Jones Industrial Average saw a rebound as it closed up at 26,403 from 25,628 a week ago. Canada’s S&P/TSX Composite Index also closed up at 16,442 from 16,037 the previous week. The S&P/TSX Venture Composite Index closed up at 589.36 from 581.95 last week.

Summary

-

Number of financings increased to 24.

-

One brokered financing was announced this week for $10.1m, a two-week high.

-

One bought-deal financing was announced this week for $10.1m, a two-week high.

-

Total dollars up to $69.3m, a three-week high.

-

Average offer climbed to $2.9m, a two-week high.

Financing Highlights

-

O3 Mining (TSXV:OIII) opened a bought deal private placement to raise $10.1 million.

-

Syndicate led by Canaccord Genuity

-

2.4 million flow-through shares @ $4.20, a 61.5% premium to the closing price on September 3rd

-

Proceeds will be used for Canadian exploration expenses in Québec.

Major Financing Openings

-

O3 Mining (TSXV:OIII) opened a $10.08 million offering underwritten by a syndicate led by Canaccord Genuity on a bought deal basis.

-

Benchmark Metals (TSXV:BNCH) opened a $7.5 million offering on a strategic deal basis.

-

Western Atlas Resources (TSXV:WA) opened a $6.4 million offering on a best efforts basis. Each unit includes half a warrant that expires in two years

Major Financing Closings

-

Filo Mining (TSXV:FIL) closed a $40 million offering underwritten by a syndicate led by BMO Capital Markets on a bought deal basis

-

Aurcana (TSXV:AUN) closed a $8.92 million offering on a best efforts basis. Each unit included a warrant that expires in three years

-

Southern Silver Exploration (TSXV:SSV) closed a $4.21 million offering on a best efforts basis. Each unit included a warrant that expires in five years.

-

Rockhaven Resources (TSXV:RK) closed a $4.07 million offering on a best efforts basis.