ORENINC INDEX - Monday, October 5th 2020

North America’s leading junior mining finance data provider

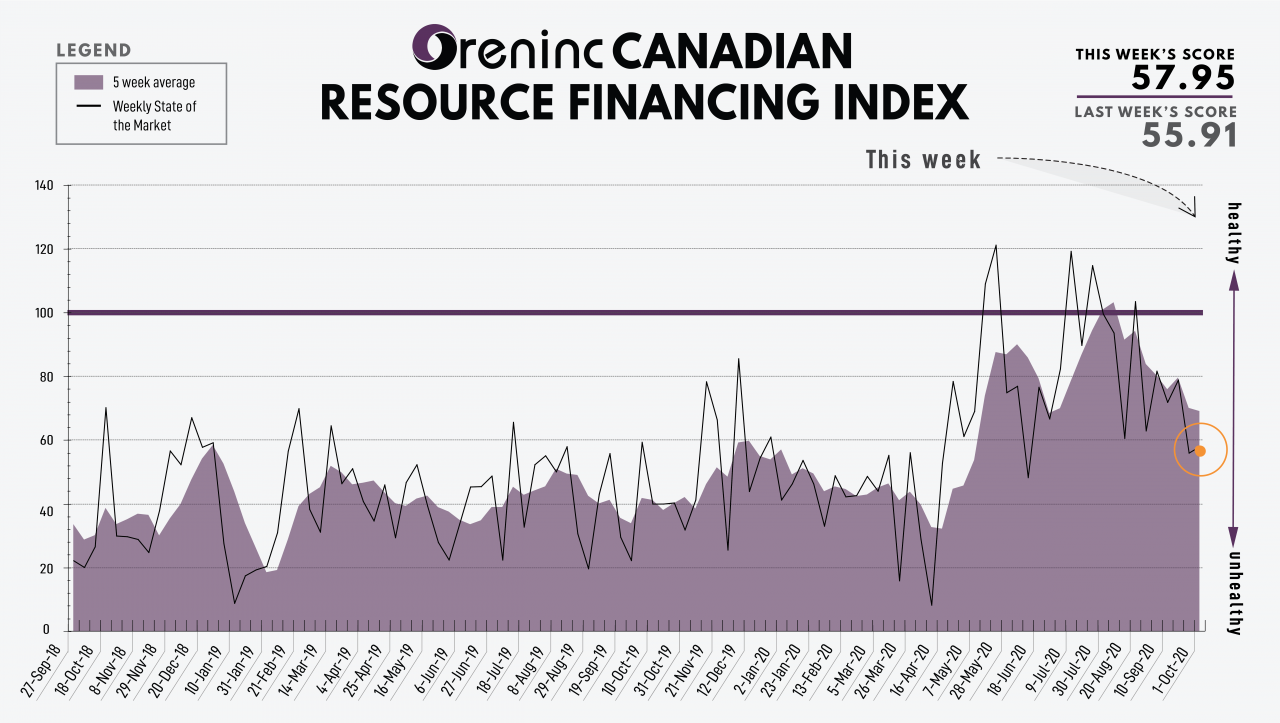

Last Week: 55.91 (Updated)

This week: 57.95

The Oreninc Index increased in the week ending October 2nd, 2020 to 57.95 from an updated 55.91 a week ago as the number of deals increased.

The COVID-19 virus global death toll has passed one million with almost 35 million cases reported worldwide.

The inevitable has happened as US president Donald Trump has tested positive for the COVID-19 virus together with first lady Melania Trump. The news came days after Trump appeared in the first debate with fellow contender in the November presidential election Joe Bidden, the Democratic Party nominee.

The US saw the number of people applying for first-time jobless claims fell 36,000 to 837,000 according to the Labor Department, the lowest reading in unemployment claims since the start of the COVID-19 pandemic. The four-week moving average for new claims was 867,250, slightly down from the previous week. Continuing jobless claims fell to 11.767 million while continuing claims fell 980,000. The Bureau of Labor Statistics later said 661,000 jobs were created in September, missing expectations of around 900,000 in job gains, as the unemployment rate fell to 7.9% from 8.4% in August.

Despite these statistics moving in the right direction, many analysts believe the recovery is still precarious and could reverse as several firms announced mass job layoffs. Walt Disney announced the firing of 28,000 workers, while 9,000 are going at Royal Dutch Shell.

Talk of a new financial stimulus package in the US continues to be just talk although House Democrats released a US$2.2 trillion proposal.

In Europe, the UK and European Union appear to be no closer to negotiation a new relationship deal. The EU launched legal action against the UK after the Boris Johnson administration failed to respond to its demand to drop legislation which would overwrite the withdrawal agreement and break international law.

Tens of thousands of jobs in the UK automotive sector are under threat due to the potential for higher export tariffs as the EU said components from Japan and other non-EU countries used on UK assembly lines should be considered British. It is thought the average British content of cars built in the UK is about 44%, which falls foul of the rules of origin system. Car manufacturer trade bodies accuse the government of doing more to protect the UK’s tiny fishing industry compared to the giant car industry.

On to the money: the aggregate financings announced increased to $95.6 million, a two-week low, which included eight brokered financings for $38 million, a five-week low, and one bought deal financing for $5 million, a seven-week low. The average offer size fell to $2.8 million, a three-week high, while the number of financings increased to 34.

A better week for Gold as the spot price recouped roughly half of the losses of the previous week to close up at $1,899/oz from $1,861/oz a week ago. The yellow metal is up 25.21 so far this year. The US dollar index weakened as it closed down at 93.84 from 94.64 a week ago. The VanEck managed GDXJ increased as it closed up at $55.32 from $54.23 week ago. The index is now up 30.90% so far this year. The US Global Go Gold ETF closed up at $22.12 from $21.82 a week ago. It is up 25.97% so far this year. The HUI Arca Gold BUGS Index also closed up at 324.54 from 320.09 last week. The SPDR GLD ETF inventory saw growth, closing the week up at 1,275.60 tonnes or 41.01 million ounces from 1,266.84 tonnes last week.

In other commodities, Silver also partially recovered as it closed the week up at $23.74/oz from $22.89/oz a week ago. Copper held the line as it closed the week even at $2.97/lb. Oil had another tough week as WTI closed down at $37.05 a barrel from $40.25 a barrel a week ago.

The Dow Jones Industrial Average moved higher as it closed up at 27,682 from 27,173 a week ago. Canada’s S&P/TSX Composite Index also nudged higher to close at 16,199 from 16,065 the previous week. The S&P/TSX Venture Composite Index closed up at 708.60 from 695.26 last week.

Summary

- Number of financings increased to 34.

- Eight brokered financings were announced this week for $38 million, a five-week low.

- One bought-deal financing was announced this week for $5 million, a seven-week low.

- Total dollars increased to $95.6 million, a two-week high.

- Average offer decreased to $2.8 million, a three-week low.

Financing Highlights

Northway Resources (TSXV:NTW) announced a best-efforts brokered private placement to raise $12 million.

- 12 million subscription receipts @ $1.00 with 25% overallotment option.

- Syndicate of agents led by Stifel GMP and including Canaccord Genuity, Haywood Securities, Laurentian Bank Securities and Echelon Wealth Partners.

- Northway has entered into an amalgamation agreement with Kenorland Minerals which will result in a reverse takeover of the company by Kenorland.

- Each subscription receipt will entitle the holder to receive one share of the resulting issuer.

- Proceeds will be used to fund exploration across a portfolio of projects in Alaska, USA and Canada.

Major Financing Openings

- Northway Resources (TSXV:NTW) opened a $12 million offering underwritten by a syndicate led by Stifel GMP on a best efforts basis. The deal is expected to close on or about October 27th.

- Benz Mining (TSXV:BZ) opened a $10.26 million offering on a best efforts basis. Each unit includes half a warrant that expires in one years. The deal is expected to close on or about October 29th.

- Aurania Resources (TSXV:ARU) opened a $10 million offering underwritten by a syndicate led by Cantor Fitzgerald Canada on a best efforts basis. The deal is expected to close on or about October 14th.

- Plymouth Realty Capital (TSXV:PH.H) opened a $10 million offering on a best efforts basis.

Major Financing Closings

- Benchmark Metals (TSXV:BNCH) closed a $50.27 million offering underwritten by a syndicate led by Sprott Capital Partners on a best efforts basis. Each unit included a warrant that expires in two years.

- Contact Gold (TSXV:C) closed a $13.54 million offering on a best efforts basis. Each unit included half a warrant that expires in two years.

- ZTR Acquisition (TSXV:ZTR) closed a $8 million offering on a best efforts basis.

Orefinders Resources (TSXV:ORX) closed a $5.5 million offering underwritten by a syndicate led by Echelon Wealth Partners on a best efforts basis.