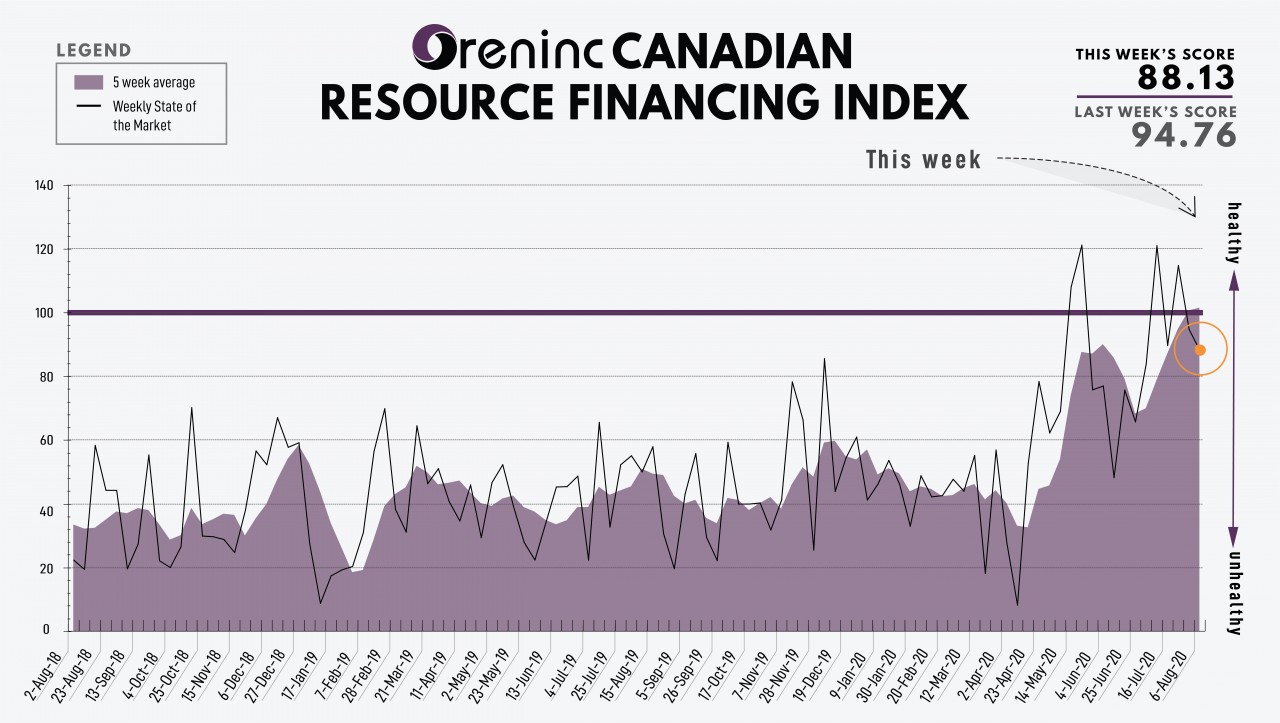

ORENINC INDEX dips as financings and brokered action falls

ORENINC INDEX - Monday, August 10th 2020

North America’s leading junior mining finance data provider

Last Week: 94.76

This week: 88.13

The Oreninc Index fell in the week ending August 7th, 2020 to 88.13 from 94.76 a week ago as financings and brokered action falls.

The COVID-19 virus global death toll has reached 725,000 with almost 19.5 million cases reported worldwide.

Gold and silver continued on a tear as the real yield on 10-year US Treasury notes hit -1% for the first time ever.

In the US, the unemployment rate fell to 10.2% as nonfarm payroll employment rose by 1.8 million in July, according to the Bureau of Labour Employment gains in the leisure and hospitality, retail trade, professional and business services, and health care sectors evidenced the reopening of the economy from COVID-19 restrictions.

The workforce participation rate remained largely unchanged at 61.4%, while total employment rose by 1.4 million in July to 143.5 million. The July unemployment rate was 10.2%, an improvement over the 11.1% rate in June. Initial unemployment benefit claims fell 249,000 to 1.19 million, while the number of people claiming ongoing unemployment benefits is 16.1 million.

Plans for a second financial bailout package in the US took a knock when the Trump administration rejected a compromise offer by Democrats, potentially creating a stand-off between the Executive and Legislative branches as the Constitution gives Congress power over finances.

On the international scene, the US and China are due to assess their phase-one trade agreement. Economic tensions between the world’s two trade powers continue to simmer with TikTok, a Chinese music video app, now in the crosshairs. US president Donald Trump said he would ban the app from the US market in September if it is not purchased by a US company before then. Microsoft is interested in acquiring the company. Trump then issued of executive orders banning any US transactions with the Chinese companies which own TikTok and WeChat in the interest of national security.

As an appetizer, President Trump announced a 10% tariff on Canadian aluminium, which saw Canada immediately retaliate dollar for dollar, some C$3.6 billion.

This past week marked the 75th anniversary of the US dropping atomic bombs on Hiroshima and Nagasaki in Japan, the only time such weapons have been used in armed conflict. The commemorations were held days after some 2,700 tonnes of ammonium nitrate—a material commonly used in fertilisers and explosives—exploded in Lebanon’s capital Beirut, killing at least 137 people and injuring about 5,000.

On to the money: aggregates financings announced pulled back to $144.6 million, a five-week low, which included two brokered financings for $33 million, a five-week low, and no bought deal financings. The average offer size increased to $2.5 million, a two-week high, while the number of financings increased to 47.

The Gold spot price had another strong week as it closed up at $2,035/oz from $1,975/oz a week ago. The yellow metal is up 34.16% so far this year. The US dollar index stopped its losing streak as it closed up a smidge at 93.43 from 93.34 last week. The VanEck managed GDXJ continued higher as it closed up at $60.95 from $60.44 a week ago. The index is now up 44.23% so far this year. The US Global Go Gold ETF pared back slightly to $24.61 from $24.90 a week ago. It is up 40.15% so far this year. The HUI Arca Gold BUGS Index closed up at 350.78 from 350.70 last week. The SPDR GLD ETF inventory continued to increase, closing the week up at 1,262.12 tonnes or 40.6 million ounces, from 1,241.96 tonnes last week.

In other commodities, Silver posted another strong week as the spot price closed the week up at $28.30/oz from $24.39/oz a week ago. Copper continued to pull back as it closed the week down at $2.79/lb from $2.86/lb a week ago. Oil returned to growth as WTI closed up at $41.22 a barrel from $40.27 a barrel a week ago.

The Dow Jones Industrial Average closed up at 27,433 from 26,428 a week ago. Canada’s S&P/TSX Composite Index closed up at 16,544 from 16,169 the previous week. The S&P/TSX Venture Composite Index increased to 739.98 from 721.24 last week.

Summary

- Number of financings decreased to 47.

- Two brokered financings were announced this week for $33 million, a five-week low.

- No bought-deal financings were announced this week.

- Total dollars decreased to $144.6 million, a five-week low.

- Average offer increased to $2.5 million, a two-week high.

Financing Highlights

Novo Resources (TSXV:NVO) announced a C$30 million brokered private placement of subscription receipts, which was subsequently increased to $42.5 million.

- Up to 13.1M subscription receipts @ C$3.25.

- Non-brokered private placement of 923,076 subscription receipts under the same terms for proceeds of up to $3 million.

- Syndicate of agents led by Clarus Securities and Stifel GMP.

- Proceeds will be used to fund the acquisition of the outstanding shares Millennium Minerals and its assets 10km from Novo’s Beatons Creek conglomerate gold project in Western Australia.

- Concurrent $60 million secured credit facility agreed with Sprott Private Resource Lending.

Major Financing Openings

- Novo Resources (TSXV:NVO) opened a $33 million offering on a best efforts basis.

- Chesapeake Gold (TSXV :CKG) opened a $20 million offering on a best efforts basis.

- Abraplata Resource (TSXV:ABRA.H) opened a $15 million offering on a best efforts basis. Each unit includes half a warrant that expires in two years. The deal is expected to close on or about August 27th.

- Ceylon Graphite (TSXV:CYL) opened a $8.1 million offering on a best efforts basis. The deal is expected to close on or about September 7th.

Major Financing Closings

- Revival Gold (TSXV:RVG) closed a $15.05 million offering underwritten by a syndicate led by BMO Capital Markets on a bought deal basis. Each unit included half a warrant that expires in 18 months.

- Royal Road Minerals (TSXV:RYR) closed a $11.55 million offering underwritten by a syndicate led by Stifel GMP on a bought deal basis.

- Summa Silver (CSE:SSVR) closed a $8 million offering on a best efforts basis. Each unit included half a warrant that expires in two years.

- Blackrock Gold (TSXV:BRC) closed a $7.5 million offering on a best efforts basis.